BOI FinCEN Form Filing

IMPORTANT INFORMATION FOR BUSINESS OWNERS: Corporate Transparency Act — Beneficial Ownership Information Reporting

UPDATE:

For the vast majority of reporting companies, the new deadline to file an initial, updated, and/or corrected BOI report is now March 21, 2025. FinCEN will provide an update before then of any further modification of this deadline, recognizing that reporting companies may need additional time to comply with their BOI reporting obligations once this update is provided.

-------------------------------------------------------------------------------------------------------------------------------------------------------

PER the FinCEN Website: Alert: Ongoing Litigation – Texas Top Cop Shop, Inc., et al. v. Garland, et al., No. 4:24-cv-00478 (E.D. Tex.) & Voluntary Submissions [Updated January 2, 2025]

In light of a recent federal court order, reporting companies are not currently required to file beneficial ownership information with FinCEN and are not subject to liability if they fail to do so while the order remains in force. However, reporting companies may continue to voluntarily submit beneficial ownership information reports.

Current Status of Texas Top Cop Shop, Inc., et al. v. Garland, et al., No. 4:24-cv-00478 (E.D. Tex.) and Voluntary Submissions

The Corporate Transparency Act (CTA) plays a vital role in protecting the U.S. and international financial systems, as well as people across the country, from illicit finance threats like terrorist financing, drug trafficking, and money laundering. The CTA levels the playing field for tens of millions of law-abiding small businesses across the United States and makes it harder for bad actors to exploit loopholes in order to gain an unfair advantage.

On Tuesday, December 3, 2024, in the case of Texas Top Cop Shop, Inc., et al. v. Garland, et al., No. 4:24-cv-00478 (E.D. Tex.), the U.S. District Court for the Eastern District of Texas, Sherman Division, issued an order granting a nationwide preliminary injunction. The Department of Justice, on behalf of the Department of the Treasury (Treasury), filed a Notice of Appeal on December 5, 2024 and separately sought of stay of the injunction pending that appeal.

On December 23, 2024, a panel of the U.S. Court of Appeals for the Fifth Circuit granted a stay of the district court’s preliminary injunction entered in Texas Top Cop Shop, Inc., pending the outcome of Treasury’s ongoing appeal of the district court’s order. Treasury immediately issued an alert notifying the public of this ruling and recognizing that reporting companies may have needed additional time to comply with beneficial ownership reporting requirements, Treasury extended reporting deadlines. However, on December 26, 2024, a different panel of the U.S. Court of Appeals for the Fifth Circuit issued an order vacating the Court’s December 23, 2024 order granting a stay of the preliminary injunction. On December 31, 2024, the Department of Justice, on behalf of Treasury, sought a stay of the injunction pending the ongoing appeal from the Supreme Court of the United States.

In the meantime, as of December 26, 2024, the injunction issued by the district court in Texas Top Cop Shop, Inc. is once again in effect. FinCEN is complying with—and will continue to comply with—the district court’s order for as long as it remains in effect. As a result, reporting companies are not currently required to file beneficial ownership information with FinCEN. Reporting companies may continue to voluntarily submit beneficial ownership information reports.

Other Updates:

Texas Top Cop Shop, Inc. is only one of several cases that have challenged the Corporate Transparency Act (CTA) pending before courts around the country.

As noted in a separate alert, on March 1, 2024, the U.S. District Court for the Northern District of Alabama, Northeastern Division, entered a final declaratory judgment, concluding that the CTA exceeds the Constitution’s limits on Congress’s power and enjoining Treasury from enforcing the CTA against the plaintiffs. As a result, the government, even in the absence of an injunction, is not currently enforcing the Corporate Transparency Act against the plaintiffs in that action: Isaac Winkles, reporting companies for which Isaac Winkles is the beneficial owner or applicant, the National Small Business Association, and members of the National Small Business Association (as of March 1, 2024). Treasury has appealed that judgment, and that appeal is pending before the Eleventh Circuit.

However, since March 2024, other district courts have denied requests to enjoin the CTA, ruling in favor of Treasury—in particular:

- On April 29, 2024, in Small Business Association of Michigan, et al. v. Yellen, et al., No. 1:24-cv-314 (W.D. Mich.), the U.S. District Court of the Western District of Michigan, denied a motion for a preliminary injunction.

- On September 20, 2024, in Firestone, et al. v. Yellen, et al., No. 3:24-cv-01034 (D. Or.), the U.S. District Court for the District of Oregon also declined to issue a preliminary injunction on behalf of plaintiffs—seven individuals—challenging the constitutionality of the CTA. In denying plaintiffs’ motion, the district court found that plaintiffs had not shown a likelihood of success on the merits with respect to their claims that the CTA exceeds Congress’ authority under the Constitution and violates the First, Fourth, Fifth, Eighth, Ninth, and Tenth Amendments. In its opinion and order, the district court noted that enjoining enforcement of the CTA “would interfere with Congress’ judgment, supported by extensive factual findings, about how best to combat money laundering, the financing of terrorism, tax fraud, and other serious crimes that affect the national economy or national security.” Plaintiffs have appealed the court’s decision, and that appeal is pending before the Ninth Circuit.

- On October 24, 2024, in Community Associations Institute, et al. v. Yellen, et al., No. 1:24-cv-01597 (E.D. Va.), the U.S. District Court for the Eastern District of Virginia likewise denied a motion by plaintiffs, including an organization that represents community associations throughout the country, for a preliminary injunction. In doing so, the district court found that plaintiffs were unlikely to succeed on their claims that (1) Congress overstepped the outer bounds of its commerce power in enacting the CTA; (2) the CTA violates the First and Fourth Amendments; and (3) the statutory exemptions in the CTA relieve community associations of the obligation to report beneficial ownership information. Plaintiffs have appealed the court’s decision, and that appeal is pending before the Fourth Circuit.

The government continues to believe—consistent with the orders issued by the U.S. District Courts for the District of Oregon and the Eastern District of Virginia— that the CTA is constitutional and will continue defending the law as necessary.

___________________________________________________________________________________

UPDATE: 2024-58: COURT PUTS BOI REPORTING ON HOLD FOR ALL BUSINESSES

December 4, 2024

A federal district court in Texas issued a nationwide preliminary injunction against enforcing the beneficial ownership reporting requirements mandated by the Corporate Transparency Act (CTA). (Texas Top Cop Shop v. Garland (December 3, 2024) U.S. Dist. Ct., Eastern Dist. Of Texas, Case No. 4:24-CV-478)

The court ruled that Congress exceeded its authority in enacting the CTA, resulting in an unconstitutional infringement on states’ rights to regulate businesses. The court granted a nationwide injunction prohibiting FinCEN from enforcing the January 1, 2025, reporting deadline for all reporting companies.

The opinion was issued on December 3, 2024, and will likely be appealed. However, for now, businesses do not have to file beneficial ownership information reports with FinCEN.

We will continue to update you as news develops on this issue.

___________________________________________________________________________________

The Corporate Transparency Act (“CTA”) was enacted January 1, 2021, as part of the National Defense Authorization Act, representing the most significant reformation of the Bank Secrecy Act and related anti–money laundering rules since the U.S. Patriot Act. The CTA is intended to address and guard against money laundering, terrorism financing, and other forms of illegal financing by mandating certain entities (primarily small and medium size businesses) to report “beneficial owner” information to the Financial Crimes Enforcement Network (“FinCEN”).

The CTA authorizes FinCEN, a bureau of the U.S. Treasury Department, to collect, protect, and disclose this information to authorized governmental authorities and to financial institutions in certain circumstances.

Our firm is sending you this communication to provide you with some general information regarding the new reporting rules, as well as initial steps you should take to address the implications of the CTA to your organization.

We strongly encourage you to reach out as soon as possible to legal counsel with expertise in this area to assist your organization with the steps you need to take to ensure compliance with the CTA, if applicable.

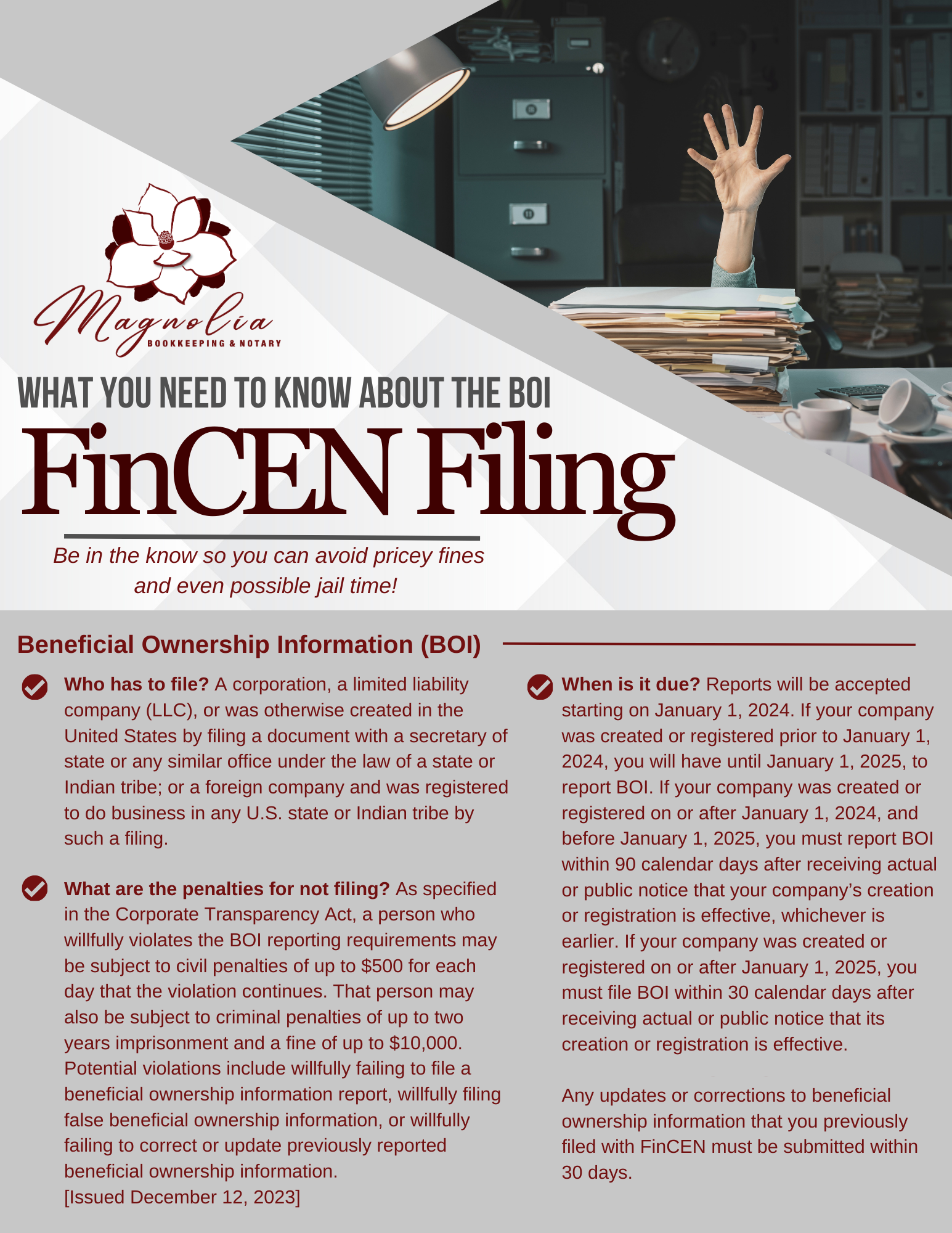

As of January 1, 2024, many LLC’s and S-Corps are required to file a Beneficial Owners Information (BOI) form with the Department of the Treasury Financial Crimes Enforcement Network (FinCEN). With this new law being passed, there will be hefty fines and even potential jail time if you have not completed this form by the deadline.

What entities are subject to the new CTA reporting requirements?

Companies required to report are called reporting companies. Reporting companies may have to obtain information from their beneficial owners and report that information to FinCEN. Entities required to comply with the CTA (“Reporting Companies”) include corporations, limited liability companies (LLCs), and other types of companies that are created by a filing with a Secretary of State (“SOS”) or equivalent official. The CTA also applies to non-U.S. companies that register to do business in the U.S. through a filing with an SOS or equivalent official. Since the definition of a domestic entity under the CTA is extremely broad, additional entity types could be subject to CTA reporting requirements based on individual state law formation practices.

There are a number of exceptions* to who is required to file under the CTA. Many of the exceptions are entities already regulated by federal or state governments, and as such already disclose their beneficial ownership information to governmental authorities.

Another notable exception is for “large operating companies” defined as companies that meet all the following requirements:

- Employ at least 20 full-time employees in the U.S.

- Gross revenue (or sales) over $5 million on the prior year’s tax return

- An operating presence at a physical office in the U.S.

Your company may be a reporting company and need to report information about its beneficial owners if your company is:

1. A corporation, a limited liability company (LLC), or was otherwise

created in the United States by filing a document with a secretary of

state or any similar office under the law of a state or Indian tribe ; or

2. A foreign company and was registered to do business in any U.S.

state or Indian tribe by such a filing.

*There are 23 exceptions to this rule; these entities include publicly traded companies, nonprofits, and certain large operating companies. FinCEN’s “Small Entity Compliance Guide” includes checklists for each of the 23 exemptions that may help determine whether your company qualifies for an exemption.

Who is considered a “beneficial owner” of a Reporting Company?

A beneficial owner is any individual who, directly or indirectly, exercises “substantial control” or owns or controls at least 25% of the company’s ownership interests.

An individual exercises “substantial control” if the individual (i) serves as a senior officer of the company; (ii) has authority over the appointment or removal of any senior officer or a majority of the board; or (iii) directs, determines, or has substantial influence over important decisions made by the Reporting Company. Thus, senior officers and other individuals with control over the company are beneficial owners under the CTA, even if they have no equity interest in the company.

In addition, individuals may exercise control directly or indirectly, through board representation, ownership, rights associated with financing arrangements, or control over intermediary entities that separately or collectively exercise substantial control.

CTA regulations provide a much more expansive definition of “substantial control” than in the traditional tax sense, so many companies may need to seek legal guidance to ultimately determine who are deemed beneficial owners within their organization.

When do you have to file?

As currently promulgated, the CTA’s reporting requirements will be phased-in in two stages:

- All new Reporting Companies — those formed or registered on or after January 1, 2024 (before January 1, 2025)— must report required information within 901 days after their formation or registration; after receiving actual or public notice that your company’s creation or registration is effective, whichever is earlier.

- All existing Reporting Companies — those formed or registered before January 1, 2024 — must report required information no later than January 1, 2025.

- If your Company was created or registered on or after January 1, 2025, you must file BOI within 30 calendar days after receiving actual or public notice that its creation or registration is effective.

Take immediate action now!

As the CTA is not a part of the tax code, the assessment and application of many of the requirements set forth in the regulations, including but not limited to the determination of beneficial ownership interest, may necessitate the need for legal guidance and direction. As such, since we are not attorneys, our firm is not able to provide you with any legal determination whether an exemption applies to the nature of your entity or whether legal relationships constitute beneficial ownership.

Since the filing of the Beneficial Ownership Report is a legal matter, we will not provide services in the area. We strongly encourage you to reach out as soon as possible to legal counsel with expertise in this area to assist your organization with the steps you need to take to ensure compliance with the CTA, if applicable.

What are the penalties for not filing?

As specified in the Corporate Transparency Act, a person who willfully violates the BOI reporting requirements may be subject to civil penalties of up to $500* for each day that the violation continues. That person may also be subject to criminal penalties of up to two years imprisonment and a fine of up to $10,000. Potential violations include willfully failing to file a beneficial ownership information report, willfully filing false beneficial ownership information, or willfully failing to correct or update previously reported beneficial ownership information. [Issued December 12, 2023]

*Note that penalties for willfully violating the CTA’s reporting requirements include (1) civil penalties of up to $5912 per day that a violation is not remedied, (2) a criminal fine of up to $10,000, and/or (3) imprisonment of up to two years.

2 The penalties for BOI reporting violations have been inflation adjusted and are increased to $591 a day from $500, effective January 25, 2024.

Where do I file?

You can file for yourself at: https://www.fincen.gov/boi OR you can reach out to a professional to assist in filing the report. If you are filing yourself, make sure to get a FinCEN ID to assit in filing prior to completing the form.

Filing is FREE. I have recorded a little video to help guide you through the form, should you need here.

How to prepare for the CTA:

With the CTA introducing a new and expansive reporting regime, now is the time to assess the new rules’ implications on your organization. Some questions and comments for your company to consider now, although not meant to be all-inclusive, include:

- Is your company subject to the CTA, or do you qualify for any of the exemptions?

- If your company is not exempt, how should you calculate percentages of “ownership interests” to determine whether any owners meet the 25%-ownership threshold? In many companies with simple capital structures, the answer will be obvious. It may be much less obvious, however, for companies with complicated capital structures (given the expansive definition of “ownership interest”), or companies in which some ownership interests are held indirectly — for example, through upper-tier investment entities, holding companies, or trusts.

- How do you assess and determine each person who exercises “substantial control” over the company? There may well be multiple people who qualify, given the expansiveness (and vagueness) of the “substantial control” definition.

1 FinCEN issued a final rule on November 29, 2023, extending the deadline for companies created or registered in 2024 to file initial beneficial ownership information (BOI) reports to 90 calendar days after their formation or registration (was originally 30 days).

- What new processes and procedures should the company put in place to monitor future changes in its beneficial owners and reportable changes on existing beneficial owners that will require timely updated reports to FinCEN? Note that the types of information that must be provided to FinCEN (and kept current) for these beneficial owners include the owner’s legal name, residential address, date of birth, and unique identifier number from a non-expired passport, driver’s license, or state identification card (including an image of the unique-identifier documentation). A word of caution, this is going to be a trap for Reporting Companies, as you will need to rely on beneficial owners to timely update you on reportable changes to their information (e.g., ownership changes, moves, marriages, divorces, etc.). As a result, a company’s operative documents may need to be revised to include provisions related to the CTA such as representations, covenants, indemnifications, and consent clauses. For example, the operating agreement may require:

- A representation by each shareholder, member or partner, as applicable, that it will be in compliance with or exempt from the CTA;

- A covenant by each shareholder, member or partner, as applicable, requiring continued compliance with and disclosure under the CTA or to provide evidence of exemption from its requirements;

- An indemnification by each shareholder, member or partner, as applicable, to the company and its other shareholders, members or partners, as applicable, for its failure to comply with the CTA or for providing false information; and

- A consent by each disclosing party for the company to disclose identifying information to FinCEN, to the extent required by law.

What is the purpose?

This notice is given under the Privacy Act of 1974 (Privacy Act) and the Paperwork Reduction Act of 1995 (Paperwork Reduction Act). The Privacy Act and Paperwork Reduction Act require that FinCEN inform persons of the following when requesting and collecting information in connection with this collection of information.

This collection of information is authorized under 31 U.S.C. 5336 and 31 C.F.R. 1010.380. The principal purpose of this collection of information is to generate a database of information that is highly useful in facilitating national security, intelligence, and law enforcement activities, as well as compliance with anti-money laundering, countering the financing of terrorism, and customer due diligence requirements under applicable law. Pursuant to 31 U.S.C. 5336 and 31 C.F.R. 1010.380, reporting companies and certain other persons must provide specified information. The provision of that information is mandatory and failure to provide that information may result in criminal and civil penalties. The provision of information for the purpose of requesting a FinCEN Identifier is voluntary; however, failure to provide such information may result in the denial of such a request.

Generally, the information within this collection of information may be shared as a “routine use” with other government agencies and financial institutions that meet certain criteria under applicable law. The complete list of routine uses of the information is set forth in the relevant Privacy Act system of record notice available at

https://www.federalregister.gov/documents/2023/09/13/2023-19814/privacy-act-of-1974-system-of-records.

According to the Paperwork Reduction Act of 1995, no persons are required to respond to a collection of information unless it displays a valid OMB control number. The valid OMB control number for this information collection is 1506-0076. It expires on November 30, 2026.

Many third-party companies are assisting in this process for a small fee. Beware of third party companies that are charging for this filing. Some are charging $200-$500 to file. It is FREE to file on your own behalf. If you have questions, please feel free to contact me at

ElizabethB@magnoliakeepers.com or

540-322-2079. You can also visit

www.MagnoliaKeepers.com anytime!

Magnolia bookkeeping- where you are not a number, we do your numbers!

FinCEN Filing Fact Sheet

Please feel free to take this fact sheet for your furture reference, and share with all your business partners and friends!